Outperforming Buy and Hold?

Long term trading methods for Bitcoin

This is not investment advice. Bitcoin is highly volatile. Past performance of back-tested models is no assurance of future performance. Only invest what you can afford to lose. You must decide how much of your investment capital you are willing to risk with Bitcoin. No warranties are expressed or implied.

Executive Summary

A dollar-cost averaged (DCA) monthly accumulation method for Bitcoin outperformed two timing strategies over a recent 4.25 Block year period. One could have almost quintupled one’s money in USD terms with equal monthly buys of Bitcoin, taking advantage of dollar cost averaging to accumulate and hold long-term.

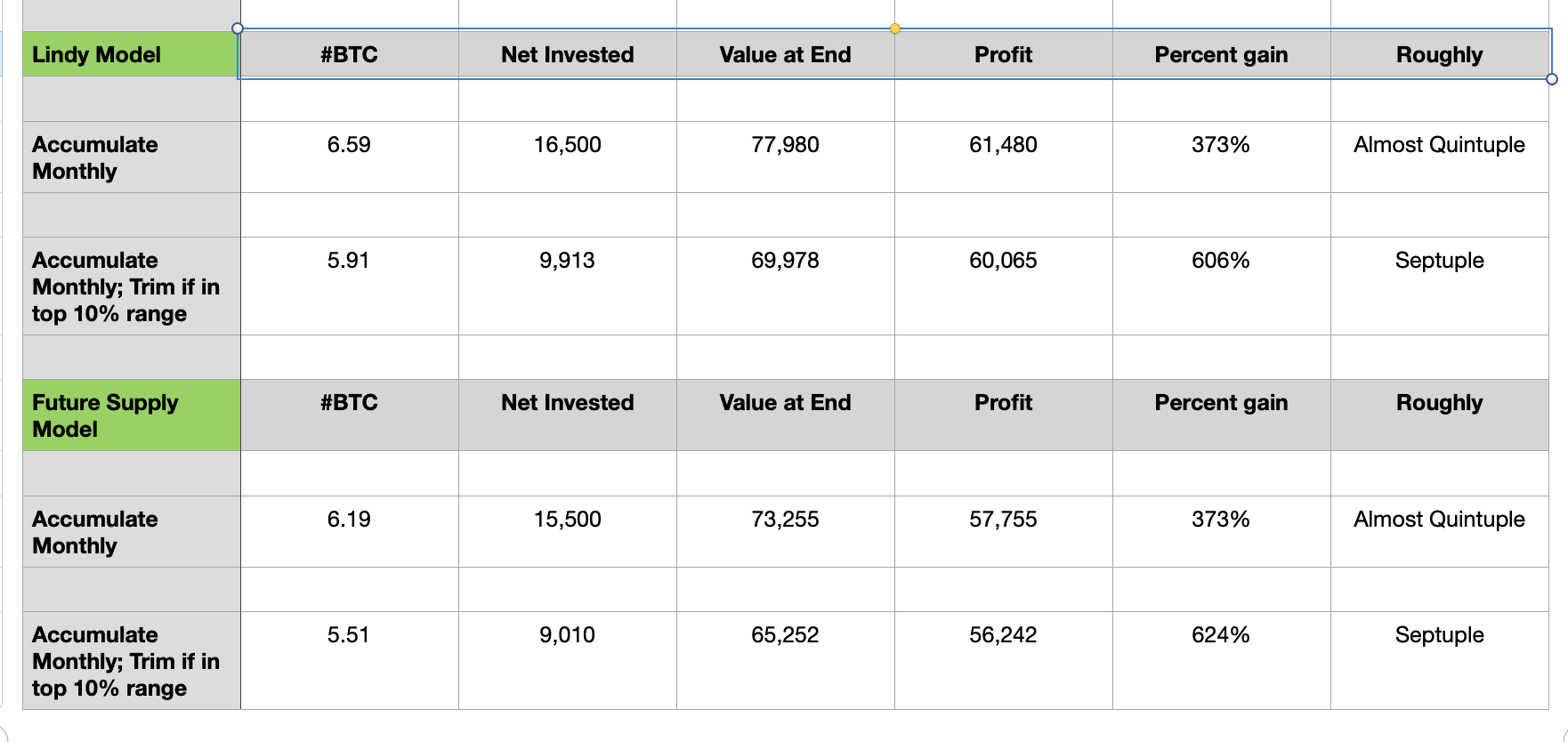

Table 1: Summary of results for 3 Trading Strategies, using two long term price models, the Lindy model and the Future Supply model.

Since Bitcoin price trends strongly upward over the long term, early buys have a very favorable impact with such a strategy. And the DCA inherent to the model means you buy much more when prices are low and less when they are high, improving the average cost basis.

By timing the buys to only occur when the price was below a model fair value, one would have done less well, only tripling the invested amount. This was true with either a Lindy Model or a Future Supply Model for the fair value price. The failure to buy early in the period decreased the return relative to the accumulation strategy.

With selective selling when Bitcoin is highly overbought relative to either model, one could have done better and quadrupled their money, better than a model based on buy signals with no sales, but even so, still not matching the simple DCA strategy.

I explore one model that can outperform the 100% accumulation strategy. The method is to accumulate 90% of the time. One sells only when in the regime of highest price deviations from model fair values, only during the most favorable 10% of the time.

Series of Five Articles

This is the last article of a five article series in which I present two long-term models for Bitcoin value. Both models exhibit positive convexity or skew to Bitcoin’s price volatility. This indicates they are Antifragile as is Bitcoin.

In the first article I provided an overview of a Lindy model of Bitcoin price vs. the block height, the number of blocks produced.

In the second article I provided an overview of my own Future Supply Model (FSM). This model is a scarcity-driven alternative to the stock-to-flow model. Whereas S2F looks at the production for a single year, the FSM looks at all remaining reserves of yet-to-be-mined Bitcoin; in other words it is the integral that matters, rather than the differential.

The third article showed that for both the Lindy model and the FSM, the residuals are positively skewed (convex). Convexity means the expected outcomes have a positive bias; the models could be favorable to trade, with potential reward exceeding risk. I also showed that a stock-to-flow model has residuals that are negatively skewed.

The fourth article was a reminder that accumulating and HODLing Bitcoin is the core strategy. Suppose you want to patiently trade a portion of your holdings using long-term signals (and never shorting Bitcoin) how could you outperform accumulate and hold?

This final and fifth article (of this series) looks at four simple trading systems and backtests over a four year period. For either the Lindy or Future Supply models the backtest results show far better results than a periodic purchase model.

Four Trading Methods

The period over which the backtest analysis was performed is from the Second Halving in July 2016 until 3 months after the Third Halving in May 2020, that is 4.25 Block years duration ending August 2020, or just over 4 calendar years. The data is on Block monthly boundaries, thus 52 months of price signals. A Block year is 52,500 blocks, a Block month is 4375 blocks, and a Block year is generally about two weeks shorter than a calendar year.

The signals for each Block month were generated using a 4 Block year lookback window, such that only historical data and backward-looking best fit parameters were used to determine each trade signal.

For each month the potential trade signals are: Strong Buy, Buy, Hold, Take profit, Strong Sell.

I examine four trading methods for the two models (Lindy and FSM). The trading strategies are:

ACCUMULATE. Accumulate regularly every month and HODL. Not really a trading method, a simple DCA dollar cost averaging method. The accumulate model bought an equal dollar amount of every month, and the amount invested was normalized to equal that from the Buy Only method, for comparison.

BUY ONLY. Buy whenever prices are lower than the model fair value. Make larger buys when prices are very low. Do nothing if price is above the model.

BUY AND SELL. Make regular buys when prices are below the model and larger buys when very low. Hold during intermediate price ranges, and sell when prices are very overextended.

ACCUMULATE and TRIM. Accumulate 90% of the time, sell only during the most favorable 10% of months.

Figure 1. Histogram of residuals for Lindy model in log10 space. We rank order these to determine the bottom 10%, bottom 50%, above the 80th percentile, and above 90th percentile levels. For example, there are 5 (out of 52) residuals above 0.6 in log10, indicating a very high price relative to the Lindy model, about a factor of 4 higher or above.

So what determines the signal? We use the residuals from the models and since they are very skewed positively we do not rely on standard deviations. Instead we categorize the residuals as follows:

Lowest 10% : Strong Buy (double usual amount) : 5 signals for either FSM, Lindy models

Price below model : Accumulate; we want to accumulate whenever the price is below model fair value : 21 or 23 signals (FSM, Lindy)

Price above model : Hold : 16 or 14 signals (FSM, Lindy)

Top 10 - 20% : Take Profit : 5 signals

Top 10% : Strong Sell (double usual) : 5 signals

The method has a bias toward accumulation, since Bitcoin is in a long-term upward trend. The buys are equal amounts unless the residual is among the 10% of lowest prices relative to the model, and then the buy is doubled. For the Buy Only model we ignore sell signals, those are treated as Holds.

The Lindy Model has two more accumulate signals than the Future Supply Model, and two fewer Hold signals. Both have 5 strong buys, 5 take profit signals and 5 strong sell signals.

The accumulate buy amounts were $500 as were the sell amounts. For strong buys and strong sells the amounts were $1000. What matters for comparison purposes is the percentage gain on capital invested.

Results for the first three methods are summarized in Table 1.Buying when below the forecast seems clever, right? You buy more when price is below the model. The problem is not that the models are no good, they have R^2 of 0.92 and 0.93 for Lindy and FSM, respectively. Their F-test and Akaike information criteria statistics show the models are useful.

The problem is the long-term trend is strongly upward, so delaying buying is sub-optimal. Even at high prices, selling can be sub-optimal.

Indeed, as shown in Table 1, the accumulate every month strategy is superior to the other two.

Perhaps you can contrive a strategy where you buy five times as much when the price is very low. But it is very difficult to ‘outsmart’ such a steep upward trend in price, despite the high volatility. Nevertheless, let’s try; that is the fourth method examined.

Accumulate and Trim

So almost all of the time we want to be accumulating. What about a strategy that buys in equal dollar amounts except when the price is extremely extended? And then we sell some of our holdings so we can prepare for new buying opportunities ahead.

I define an accumulate and trim strategy as one that buys every month 90% of the time, and only sells 10% of the time when price is very overextended. Relatively simple.

As shown in Table 2, for the Lindy model with the Accumulate and Trim strategy we end up with 5.91 BTC instead of 6.59, our profit is nearly the same, but our net investment is much lower at $9913 rather than $16,500. Thus the percent gain is 606% rather than 373%.

With the FSM model we do slightly better. The profit is nearly the same on an invested dollar amount that is 42% lower, resulting in 5.51 BTC at the end rather than 6.19 and a 624% gain rather than 373%

Both of these strategies more than septuple the investment, outperforming the straight accumulate model by factors of 1.63 and 1.68 in percentage gains.

Table 2: Summary of results for Accumulate and Trim strategy, using the two long term price models. It substantially outperforms the dollar-cost averaging accumulate only strategy by selling at extreme price excursions in the top 10% as informed by the price models.

To recap, one buys in equal dollar amounts every month, and sells only in months with prices in the top 10% highest residuals away from the model forecast. In this backtest those came one after another essentially, with five sell months in a six month interval during the late 2017 / early 2018 price spike.

The sells were sized to reduce the total stake invested by about 40%. One could adjust depending on what size you want for your core holding that you don’t plan to trade.

The main risk for the strategy is that the shape of the residual curve changes due to reduced volatility of Bitcoin, long right tails ameliorate, and you miss a few selling opportunities. But in that case you could still make a lot of money, even though missing signals, since you are using the accumulation strategy as the core of the approach.

And eventually there will be additional top 10% excursions since that bin is defined relative to the other residuals.

As an outstanding savings vehicle, Bitcoin is a game of patience and low time preference.

Portfolio Management

How much of your overall portfolio should be in Bitcoin? That is a complex question. Even a few percent has been shown to provide substantial benefit to improved returns and higher Sharpe ratios.

In a future article I will look at a Kelly-optimized portfolio management method for hard assets: between gold and Bitcoin. What is the optimal portfolio mix? Thomas Cover’s (Stanford professor, deceased) universal portfolio technique can provide an answer.

Please let me know in a comment regarding your trading style, do you just buy and HOLD, do you set price objectives? Are these models helpful?