Flash Hash Crash: have we peaked?

And is Bitcoin a Ponzi scheme?

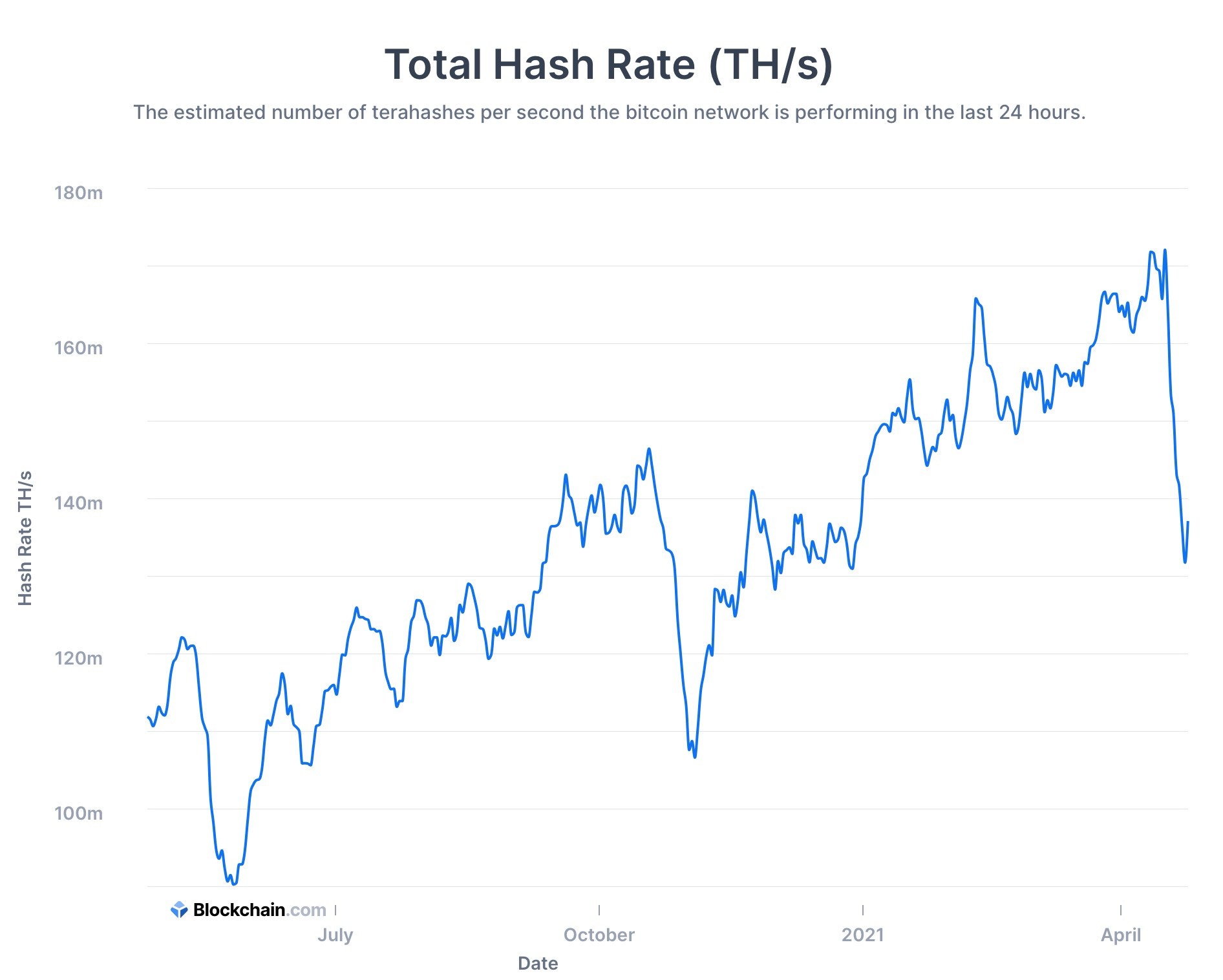

Figure 1. Bitcoin total hash rate, 7-day average, over the past year (blockchain.com)

This is not investment advice. Bitcoin is highly volatile. Past performance of back-tested models is no assurance of future performance. Only invest what you can afford to lose. You must decide how much of your investment capital you are willing to risk with Bitcoin. No warranties are expressed or implied.

Flash Crash Causes

Bitcoin had a flash crash on April 18. There have been several reasons given. A coal mining accident a few days prior led to shutdown of Bitcoin mining in Xinjiang province. In Xinjiang miners use an electricity mix of largely coal or hydropower, depending on the season. The recent shut down of the mine for safety inspections led to power blackouts and mining hash rate dropped considerably.

It has been hypothesized, and is reasonable to consider this as one significant reason for the flash crash in price.

The above chart shows the 7-day average hash rate. The total hash rate dropped from over 170 Exahashes (170 million Terahash/s) to close to 100, since so much mining happens in China, especially in Xinjiang and Sichuan. The latest hash rates have already recovered to about 160 EH/s.

Cause #2?

Attacks on Bitcoin’s energy usage from ESG community have ramped up recently, especially around Earth Day on April 22nd. One example is the Bank of America’s recent white paper; see my response here. But Bitcoin mining, although over a million mining rigs are emplyed, is much less than 1% of global electricity usage.

One must understand that Bitcoin mining has produced long-lasting value, a permanent ledger of over a million mostly high-value transactions per week and a trillion dollars of monetary asset value. The US financial industry (that Bitcoin and cryptocurrency seek to overhaul) accounts for 21% of GDP, and consumes a huge amount of electricity and computer power for moving money around, and not principally for production of value.

Bitcoin is moving toward the most efficient energy frontier of renewables, using large amounts of hydropower in China and North America, especially, and now miners are even capturing flared gas in the field in North America and elsewhere. Bitcoin miners are very flexible, moving their location to cheaper energy regularly, and also entering into load-balance agreements with utilities, which helps support solar and wind development.

Cause #3?

Nicholas Nassim Taleb (financial guru and the author of Black Swan and Antifragile) has been on CNBC and tweeting recently calling Bitcoin a Ponzi. His basic argument is it is too volatile to be a currency, but that doesn’t mean it’s tulips as he suggests. In fact he concedes it could go to $1 million in value per Bitcoin.

It is not a Ponzi, and unlike our debt-based monetary system, it is an asset of slowly growing supply, with a monetary technology Lindy effect manifesting for over a dozen years now. Here is the definition of a Ponzi, from Merriam-Webster:

an investment swindle in which some early investors are paid off with money put up by later ones in order to encourage more and bigger risks.

But there is no swindle, no one paying off early investors with new money, people buy and sell the asset freely of their own volition, just as they do gold, say, or fine art. Anyone who bought and held at any time since Bitcoin began in 2009, and prior to February 19th of this year, is sitting on a profit. The whole modus operandi of a Ponzi scheme is to manufacture new shares of something as fast as you can convince people to buy them. Bitcoin has no company or organization, no commissioned sales people, and the supply issuance gets tighter every year.

Cause #4?

There were rumors of US. Treasury FINCEN enforcement actions against exchanges and other operators in the cryptocurrency space for money laundering violations. These are yet to be confirmed, perhaps some hedge fund wanted to enter at a lower price.

A typical pullback

The price drop is really a blip when looking on even just a one year time scale. A year ago the price was less than $10,000 and this recent drop was around 25% from a peak of about $64,600 on April 14. Bitcoin has experienced many such drops and always recovered over time. Now it has recovered somewhat to about $52,500.

Yes bitcoin is volatile, but its volatility is a feature not a bug, it is opportunity as well. Volatility in Bitcoin is skewed to the upside, which means it is a convex asset. Taleb has extolled the virtues of convex and anti fragile assets. Indeed, I have written a blog on the antifragile nature of Bitcoin, inspired by my reading of Taleb’s book titled Antifragile.

So where do we stand now?

Figure 2. One year chart of Bitcoin price in USD (blockchain.com). In the last day the price has turned around, reaching above $52,000.

Four Models

Over the years I have developed several models for Bitcoin’s price and market cap and also followed popular models, in particular the Stock-to-Flow model. I have critiqued the stock-to-flow model as unrealistic in the long term since it grows as a power law of an exponential, but for now it is performing well.

All models are wrong, some are useful.

I prefer to evaluate models in block time, the natural time for the Bitcoin blockchain, since the halvings at each 210,000 blocks are important “shock-to-flow” drivers for Bitcoin’s price. A roughly four year halving interval is evident as a cycle in Bitcoin’s price over time. Also the difficulty adjustments that respond to growing hash rate occur on regular intervals of 2016 blocks and work as a feedback mechanism to incentivize increased hash rate and security.

A Block year is just one quarter of that halving interval, or 52,500 blocks. A block month is 4375 blocks (all have equal length). Block years run a little bit shorter than regular year, by about two weeks, since the average block times are a bit shorter than the 10 minute target. The fortnightly difficult adjustments (each 2016 blocks) increase the needed hash rate for successful mining and steadily push the time back toward the 10 minute reference duration for a block.

Lately I have been tracking four models with block monthly data extended over a decade plus:

A simple exponential of block years, P ~ exp (a*B), where B is time in block years and P is price

A Lindy power law in block years, P ~ B^k (k is non-integral)

A stock-to-flow model regressed in block years, P ~ S2F^k where S2F is a well-defined monotonic function of B

A Bitcoin vs. gold exponential model in calendar years. This model uses Bitcoin priced in ounces of gold.

One could look at the first three (and even the fourth) in either price or market cap terms. Given the large variation in the models it is easier to just do regressions in price.

In Table 1 below the first column gives the type of model and the second column the best fit slope or power law index parameter for the regression. The third column gives the current model fair value, followed by columns for one year and four year future estimates of fair value. The sixth and seventh columns give the corresponding one and four year expected gains in fair value. The eight column gives the R^2 value for the regression and the next to last column the standard deviation of the log base 10 for the price. The final column gives the Z-score, or number of standard deviations by which the current price of $50,000 exceeds the model prediction.

The fifth row provides the geometric mean for the three models for fair value and the forecast model values and expected gains on a one year and a four year timescale. So it is a composite model. Also shown are the average of the standard deviations for the three models and the resultant Z-score for this composite model.

One sees that all of the first three models have similar R^2. The Lindy or power law model performs best in R^2 and also in comparison with the F-test. It has the lowest standard deviation of the three. All models have fair values below the current price, especially the Lindy model. The Z-scores for the current $50,000 price range from slightly above the model to 1.59 standard deviations above in the case of the more conservative Lindy model.

The exponential model has the highest one-year objective, since stock-to-flow changes only slightly between halvings and that model increases by only 5% over the next year. It also has the highest four-year objective as well, even though stock-to-flow predicts a price in excess of $300,000, the exponential model would exceed $1 million per Bitcoin.

The exponential model has the price increasing a factor of 10 every 2.76 Block years, while the stock-to-flow model increases about a factor of 8 every 4 Block years. The Lindy power law model would take about 7 years for price to grow a factor of 10.

Please note that all of these models will fail in the long run. Trees don’t grow to the sky, and yes Bitcoin may go to the Moon, but there is a finite amount of wealth, around $400 trillion globally including real estate, stocks, bonds, commodities and more. Not all of this can find its way into Bitcoin. The US money supply is just a fraction of wealth in the country. At some point the long-term price curve has to flatten out, as we discuss with these S-curve adoption models. We don’t know if Bitcoin’s price rise will saturate around $10 trillion in current dollars (digital gold narrative) or $100 trillion (global M2 money supply narrative) or somewhere else.

But for now we are in the fast rising part of the curve and these models might be useful. In fact one can show mathematically that in early times the Weibull functional form for an S-curve reduces to a Lindy style power law model.

Table 1: For each of the three Bitcoin vs. USD models we give the slope/power law index, model fair value and one year and four year forecasts. We also show the R^2 and standard deviations and Z-scores for these models. A composite model is shown below these, and in the bottom row a Bitcoin exponential model as measured in ounces of gold.

Looking at these models and the recent drop, the conclusion is: Don’t panic! There are large potential gains ahead. Price is stretched a little bit, depending on the model, but not that much when you consider that standard deviations are large, over a factor of two in linear terms.

And note that a drop in prices to as low as around $18,000 for the most optimistic exponential model would imply a not very unusual Z-score of -1 and thus would still not destroy the long term validity of the model. Such a price would still have a positive Z-score with the Lindy model. It would properly be perceived as a very favorable long-term buying opportunity.

In this article I discuss how it is very difficult to outperform dollar cost averaging combined with long term HODLing. And in this article I looked at the Kelly optimal fraction for Bitcoin in a two-asset portfolio with USD, suggesting one might want to hold as much as 1/3 of wealth in Bitcoin. Of course this is a very simplified analysis and one needs to consider other portfolio holdings and how they correlate to Bitcoin.

Over the long term Bitcoin has proven to have low correlation with almost all non-crypto assets, and this is one motivator for institutional adoption, which is small, but growing rapidly. You can still front run banks and institutional money as an individual investor.