Bitcoin and Ethereum Portfolio Allocation

A Kelly Capital Growth Analysis

This is not investment advice. Bitcoin and Ethereum are highly volatile. Past performance of back-tested models is no assurance of future performance. Only invest what you can afford to lose. You must decide how much of your investment capital you are willing to risk with Ethereum or Bitcoin. No warranties are expressed or implied.

Ethereum benefiting from DeFi

Ethereum has been on a tear lately, just passing $4000 within the past week. It has been benefitting from the boom in DeFi, including NFTs, and heightened interest in the roll out of Ethereum 2.0, which will occur in multiple phases. Ethereum liquidity on exchanges has dropped by some 27% over the past year, according to an article by Sarah Tran on FXStreet.

One well known Macro guru says his hedge fund friends are pivoting to Ethereum from Bitcoin. Maybe it’s a trade, but what about for the longer term investor?

An improvement proposal due to take effect in two months’ time as part of the London upgrade will tighten supply issuance via burning of fee tokens, and a look at this week’s transaction fees suggests the tightening could be substantial. It could even possibly flip a disinflationary (slowing inflation) cryptocurrency into absolute deflationary territory if it persisted. Note that only base fee tokens and not ‘tip’ tokens will be burned.

Maybe there’s a trade until the burning kicks in, and after that, from a stock-to-flow perspective it depends on whether the burn rate achieved exceeds expectations or not.

Another change, sharding, will help scaling for the overburdened main chain. By far the largest uncertainty ahead is the planned shift to Proof of Stake and away from the current Proof of Work consensus.

That shift could undercut the blockchain’s security. It looks to increase centralization, since the minimum staking amount is 32 Ethereum, over $100,000. Proof of Work is the proven method to ensure the security of transactions by incentivizing a higher mining hashrate. High hashrate enhances the store of value attribute for a cryptocurrency and the capital and operating costs of mining tend to place a floor under the price.

Ethereum hitting new highs in USD but not in BTC terms

Currently Ethereum’s supply inflation is 4.3% (stock-to-flow of 23) while Bitcoin’s is 1.75% (stock-to-flow of 57). So from a monetary hardness perspective Bitcoin is more like gold, amd Ethereum more like silver. Also, Ethereum’s future monetary policy is not algorithmic like Bitcoin’s, but is subject to human input from developers and the community.

In an article at the end of last year, I said the historical price action over the prior four years did not justify any significant allocation to Ethereum in a two-asset Bitcoin and Ethereum portfolio, according to the Kelly capital growth criterion. https://stephenperrenod.substack.com/p/ethereum-or-bitcoin

At the time of that article Bitcoin (BTC) was priced at $26,939 and Ethereum (ETH) was priced at $703, around 2.6% of the Bitcoin price. The respective market caps were $499 billion and $29 billion respectively.

As of May 14, BTC is $50,760 and ETH has reached $4066, or 8% of Bitcoin’s price. This is more than a doubling in relative terms in the past 5 months. The respective market caps are now $950 billion and $471 billion, so Ethereum’s market cap is 43% of Bitcoin’s. Talk of a ‘flippening’ has re-emerged, the (mythical?) idea being that Ethereum’s market cap could at some point surpass that of Bitcoin.

Figure 2: Chart of first of month price of Ethereum relative to Bitcoin from January, 2017 until May, 2021. The price has ranged from about 0.01 to about 0.11 with a mean of about 0.04 BTC. While there are trends apparent over time scales of a few months to a year, linear regression shows no overall long term trend.

Kelly analysis for ETH and BTC only portfolio

In this article, I extend the Kelly capital growth criteria analysis to incorporate the last several months of price history for the two cryptocurrencies. Also, I use more data, with monthly sampling of price rather than quarterly. And I examine three asset portfolios that include ETH, BTC, and cash (USD).

Ethereum only began in mid-2015; I look at monthly data across two time frames: (A) since the start of 2017, some 52 months’ of returns (4.3 years), and (B) a 3-year (36 month) window starting from May 2018.

The figure above charts the first of the month price of Ethereum since January 2017. One sees an upward trend for the first half year followed by a very volatile declining period until early 2020. For the last year and a half Ethereum has been mostly outperforming Bitcoin.

However, overall there is no trend. A linear regression yields a slope of -0.01, an R^2 of only 0.22, and an average price of 0.41 BTC for ETH. One could say in general that ETH is in a very broad trading range and has yet to exhibit a new high against Bitcoin. That would require ETH to move above $7000 if BTC were unchanged.

Using the Kelly capital growth criterion, I evaluate a two asset portfolio, and look at each month to see whether Bitcoin or Ethereum ‘won’ that month, and by what percent.

Table 1. I look at a series of 52(36) one-month returns of Ethereum relative to Bitcoin. The percentage of wins (losses) and average win (loss) size feed into the Kelly formula. The factor b is the ratio of win magnitude to loss absolute magnitude, and f = p - q/b is the optimal Kelly fraction in a two asset portfolio (note that in the ‘no edge’ case p = q = 0.5 and b = 1, f = 0 and you commit no capital to the asset, if f is negative a short position could be considered).

There is significant variation in the results depending on whether the 3-year window or 52-month window is used. For the shorter window an allocation of just 3.6% to Ethereum relative to a Bitcoin position is the result. But for the longer time frame, including 10 data points above 0.6, a two-asset portfolio of 27% Ethereum and 73% Bitcoin is suggested.

It must be remembered that these are fractional allocations within a two-asset crypto sub-portfolio and are not percentages for a complete portfolio that also holds non-crypto assets. Previously I have calculated a full Kelly allocation for Bitcoin of around 33% of a portfolio containing only USD cash and Bitcoin: https://stephenperrenod.substack.com/p/kelly-capital-growth-criterion-for .

Some may ask why not go all-in on Bitcoin, why not allocate 100%? It’s the extreme volatility; don’t be foolish. The Kelly method assumes continual rebalancing in the portfolio and maximum growth occurs by maximizing the logarithm of wealth over time. The Kelly technique risk manages volatility to avoid risk of ruin, and with the rebalancing forces one to accumulate Bitcoin when prices are lower than trend. Although Bitcoin’s price increases strongly over time (Ethereum’s also, apparently) there are many down months and a large cash position provides dollar cost averaging opportunity.

Summary of two asset portfolios

So maybe now you are thinking what about a three asset portfolio with USD or other fiat, BTC, and ETH? It gets complicated because BTC and ETH are well correlated. The correlation of monthly returns over the 52 month period is a positive 0.52.

This moderate degree of correlation suggests that one could add some ETH to a USD and BTC portfolio to improve returns and hedge risk to some extent as well.

In the Table 2 below we summarize results for three two-asset portfolios followed by three three-asset portfolios. And for each of the six portfolios we show both a three-year time frame and a 52-month time frame (4.3 years).

Shown are the win fraction p, the average win to average loss ratio b, and the resulting full Kelly optimal percentage, as well as the expected average monthly return, assuming monthly rebalancing. We also show the USD cash position and summarize the approximate USD/BTC/ETH percentages.

The first two-asset portfolio is ETH and BTC, and it shows that one would have gained 6.67% per month, in Bitcoin terms with a 27% fractional allocation to ETH over the longer time period. The recent 3-year timeframe suggests a very small allocation to ETH would be justified, however.

For a two-asset ETH/USD portfolio one could in principle have averaged 20% (5.66%) per month (almost 800% per year) over the longer (shorter) time period. Over the longer time period the allocation to ETH would have been quite high at 46%. You likely won’t do this well; remember to realize results like this requires a constant rebalancing of the portfolio to the optimal f value. This can imply substantial capital gains tax consequences.

For a two-asset BTC/USD portfolio one could in principle realize an 15.6% average per month over the long time period, and almost 9% monthly was found for the shorter time period. The results suggest an allocation of up to 39% to BTC in a two asset portfolio.

Three asset portfolios

For three asset portfolios including USD, BTC, and ETH, I consider three possible BTC to ETH ratios in the crypto portion of the portfolio, and then perform a two asset Kelly criteria evaluation for the merged crypto portion against USD. This is done using the appropriately averaged returns for each specific BTC:ETH ratio. The three possibilities are equal amounts of BTC and ETH, or either twice as much BTC as ETH, or three times as much BTC versus ETH.

All of the portfolios look good, but with much higher expected returns using the data from the longer time frame. In that case each has a monthly expected return of around 20%. For the shorter time frames, the expectation is around 8% per month.

It does seem like an allocation of up to half as much Ethereum as your Bitcoin holdings is favorable in historical terms. The more Ethereum allocated, the larger the spread in returns as can be seen from the variation in 3 year and 4.3 year window results.

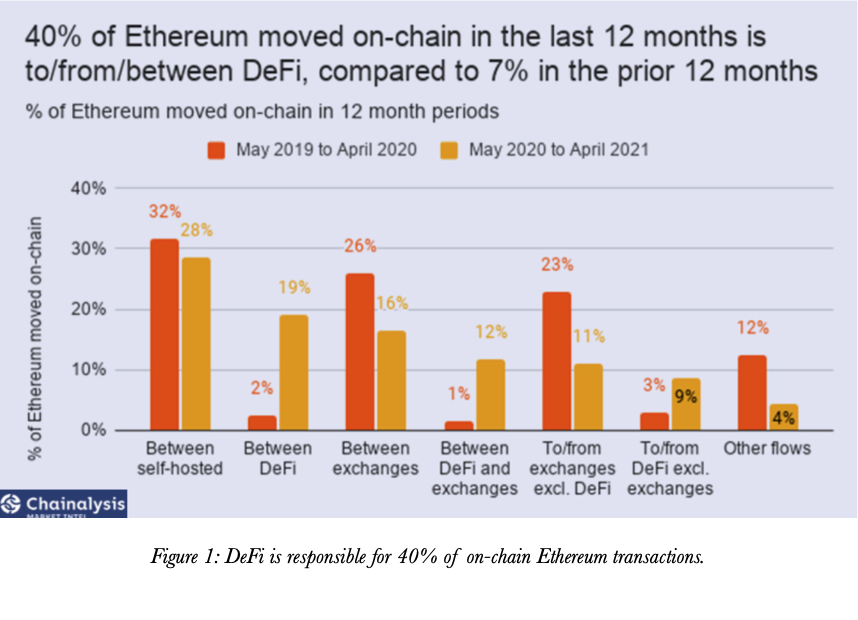

There is no doubt that ETH is more volatile (just look at Figure 1) with a maximum loss in a single month observed to be -54% vs. the USD, over the 4.3 year period, much more than BTC’s already highly volatile maximum single month loss of -37%.

Yet given the relatively flat surface as one moves from 1:1 to 2:1 to 3:1 for the BTC to ETH ratio, it looks as if one could be rather lazy about rebalancing, which is good from a tax liability perspective.

The big forward uncertainty is the planned shift to Proof of Stake, away from Proof of Work consensus mining. This would be the Serenity move from Ethereum 1.5 to Ethereum 2.0, and it may happen by the end of 2021. No one really knows, this change already missed a 2020 deadline. And no one knows if the air will go out of the Ethereum balloon once the burning of fees modification kicks in, and the move to proof of stake has happened.

What we do know is that Ethereum fees are very high now and the modification will burn tokens in the amount of one type of fee, the base fee, but will not burn the other type. The second type is a ‘tip’ fee to miners that will push your transaction to higher priority. There is a split in the mining community, with some pools supporting the change and others opposing it, see https://stopeip1559.org/. Miners will collect lower fees, but will also continue to collect the block reward of 2 ETH.

This article argues that Ethereum’s valuation could improve considerably https://softmax.substack.com/p/5k-ether-price-target-after-ethereum-2-upgrades if future burning lowers future supply considerably. But we do not know if it will cut the supply inflation rate from 4% to 2% or to 0% or even make Ethereum deflationary. Time will tell.

From a Pareto principle or 80/20 rule standpoint, Bitcoin is 80% store of value, and 20% medium of exchange, and Ethereum is the opposite, much more a medium of exchange, by its very design, than a store of value. The move to Proof of Stake could well push it further in that direction, undercutting the store of value attribute.

While one can value Bitcoin by its stock-to-flow history, that does not work statistically for Ethereum, which also has no clear supply formula. It is more like a payments processor such as Visa. Perhaps it can be modeled on its transaction volume, along with its unpredictable supply. Market cap would be some function of fees collected.

As I wrap up this article, Bitcoin’s share of the entire cryptocurrency market cap is 41% and Ethereum’s 20%; that may inform some people’s relative allocations.

Question:

1. Why would someone consider a 1-99 Bitcoin to Cash portfolio (crypto barbell strategy), when a 40-60 portfolio is clearly better? Is it merely for clickbait value?

2. Is it possible to add bonds, gold/silver, and stocks to this analysis, and see how this goes?