This is not investment advice. Bitcoin is highly volatile. Past performance of back-tested models is no assurance of future performance. Only invest what you can afford to lose. You must decide how much of your investment capital you are willing to risk with Bitcoin. No warranties are expressed or implied.

Bitcoin is that solid long-term savings vehicle, for people with low time preference, with a long-term investment horizon. It is not designed, it was not designed by Satoshi, for twitchy fingers. It was designed because the Money 2.0 fiat system is increasingly creaky; it rests on weak foundations. And Bitcoin was designed because the technology made it possible to create a new and better Money 3.0 for the 21st century.

It is not enough to look at the CPI or personal consumption expenditure (PCE) deflator that the Fed uses, when evaluating inflation. It is not enough to hear from the Fed that they are targeting 2% inflation, and falling behind, and accept that as truth.

One should look at the actual monetary aggregates themselves. Money does not always flow into the real economy, sometimes, like now, it flows into assets. Increases in the money supply may be offset by improvements in productivity and by technological progress that creates new products and lowers prices on existing ones, offsetting some of the consumer inflation that would otherwise occur.

Money may flow into stocks or bonds or real estate instead (asset inflation) but in the case of stocks there are only so many names for people to chase. In a time of interest rates near zero, like today, stocks can rise to excessive valuations.

Since Bitcoin has a predefined supply schedule, we can compare it against the money supply, and in this case I choose the M1 measure for US dollars as recorded by the Federal Reserve Bank of St. Louis (FRED app).

It is more appropriate to compare Bitcoin to the M1 money supply than the broader M2, since Bitcoin is highly liquid, and M1 is the most liquid measure of retail money (monetary reserves are held only by banks and the Federal reserve).

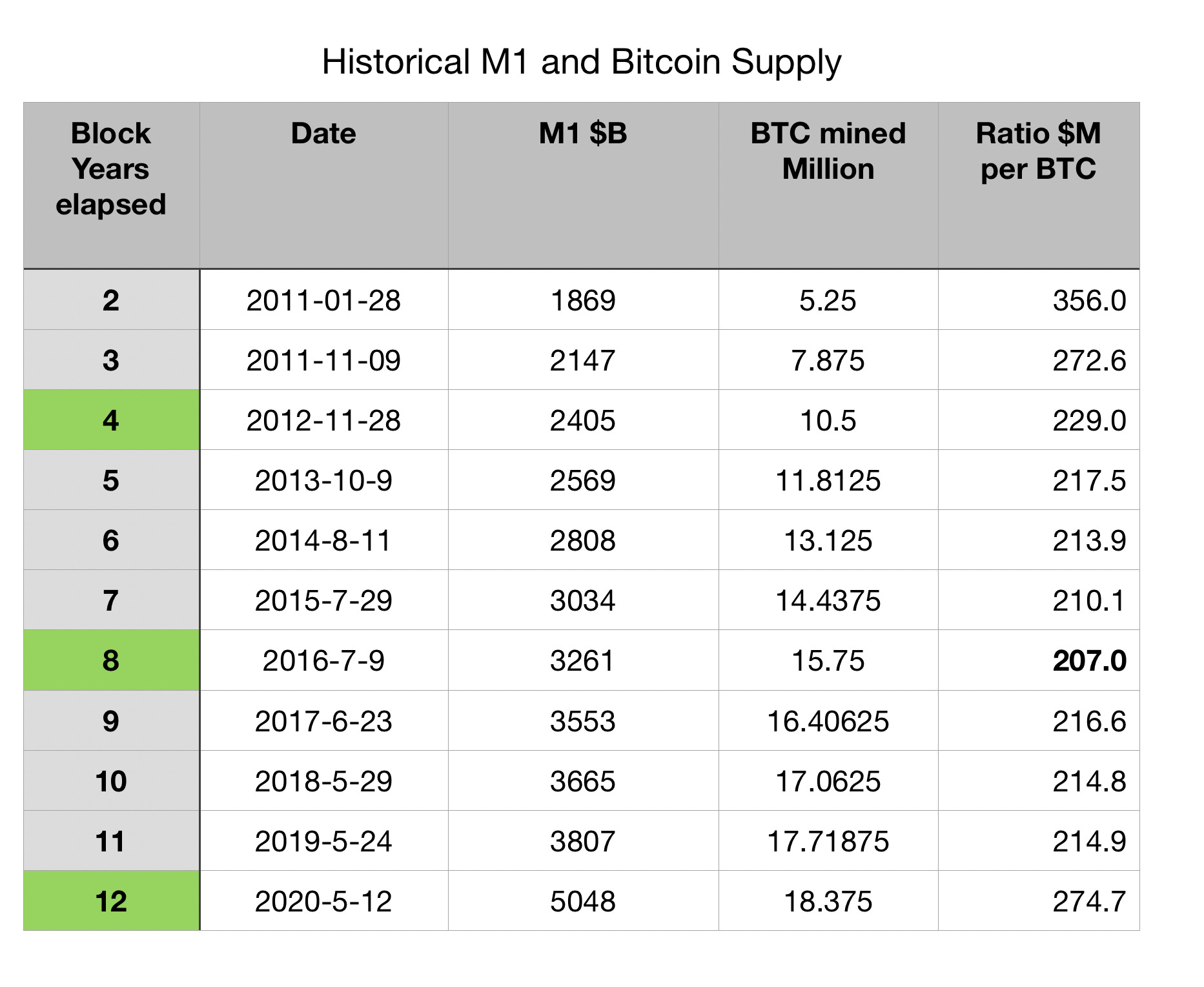

M1 Supply and Bitcoin Supply History

In Table 1 I show the M1 and Bitcoin money supplies (total number of Bitcoin minted as of the date in question) over the past 10 Block Years. Each Block Year consists of 52,500 blocks of approximately 10 minutes’ duration, and is somewhat shorter than a calendar year. The table shows the calendar year dates as well as the elapsed number of Block Years.

Each four Block Years (shaded green) there is a Halving event which cuts the Bitcoin supply issuance in half, so one can see the supply grow more slowly subsequent to each Halving.

Table 1. For Block years elapsed from 2 to 12, we tabulate the M1 money supply in billions of USD and the total number of Bitcoin minted. The final column provides a ratio of the M1 supply in millions of dollars per Bitcoin. For the first 8 Block years the Bitcoin supply was inflating more rapidly than M1, but from then on its supply has grown more slowly than M1. Note the big jump in M1 from 11 to 12 Block years elapsed due to the COVID-19 recession relief response in the spring of 2020 by the Fed and Congress.

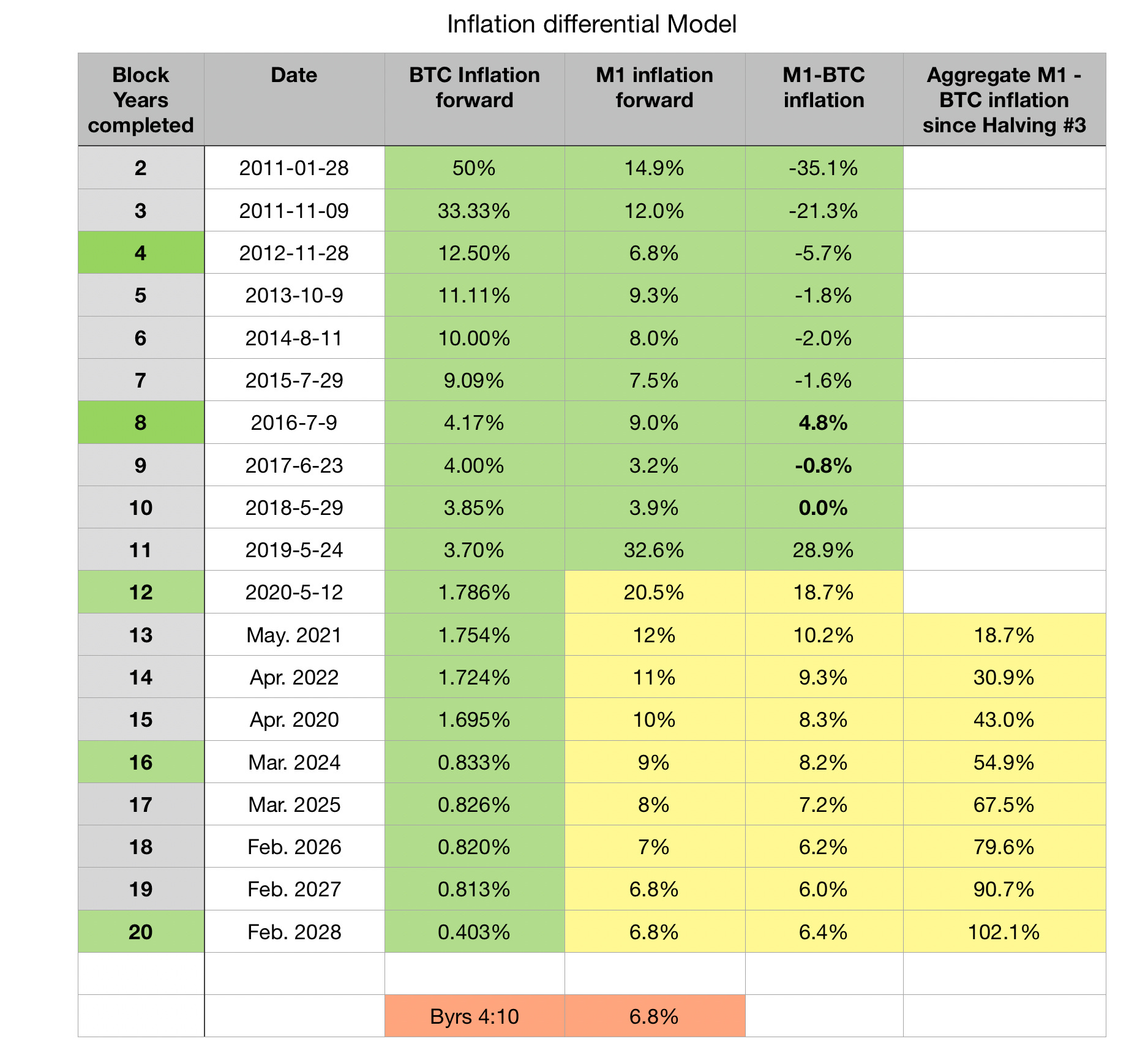

An M1 Scenario for the next 7.3 Years

In Table 2 we tabulate the Bitcoin one-year forward looking inflation at the beginning of each new Block Year (thus 2 Block Years row tabulates the algorithmically coded Bitcoin inflation for the newly entered 3rd year of Bitcoin). We also tabulate the one Block year forward inflation for the M1 supply historically, and then use a plausible model for M1 inflation between now and early 2028 (Block Year 20 start).

Estimated quantities are highlighted in yellow. For M1 inflation we assume the rest of this Block year is similar to the prior quarter after a big stimulus surge in the spring, but that there will be substantial additional stimulus in the new year.

We also assume a more rapid growth of M1 than usual for the next few years before tapering off to the 7 year average of 6.8% which characterized the period between the Great Recession and the COVID-19 Recession. So we can compare Bitcoin’s ever-lessening inflation to the substantial M1 inflation expected in this particular scenario, and we show the differential between the two in the table.

The final column of this table shows the cumulative relative inflation compounded forward between the May 2020 Halving and early 2028. Essentially the M1 money supply could double relative to the Bitcoin supply during the next 7-1/3 years.

Table 2. Bitcoin’s inflation rate in the future is completely determined by the Nakamoto consensus protocol and Halving schedule. By 2024 its inflation will drop below 1% forever and by 2028 below 1/2% with its inherently disinflationary supply algorithm. The M1 money supply growth going forward is highly uncertain, we have a big COVID-19 shock upwards after 11 Block Years elapsed. I have assumed more extraordinary stimulus the next few years, as occurred following the Great Recession and then a taper back to a more typical growth just below 7% per annum. The fifth column shows the difference between M1 and BTC inflation. Bitcoin has been harder money since it was 8 Block years old with the second Halving in mid-2016.

All other things being equal, one might expect Bitcoin’s price in US dollar terms to double as well.

Today the price is $12,750 and a 102.1% increase would be to $25,844, a compound annual rate of 10.1%. And at the end of that period one would essentially be holding a perpetual zero coupon bond with implicit yield return nearly equal to the M1 inflation rate in high single digits or more.

That is not too shabby at all in these days of sub-one percent interest rates on the 10-year Treasury.

And that does not allow for greater adoption of bitcoin, by retail investors and corporate treasuries such as Microstrategy’s $425 million investment, and by investment funds. And ease of use and entry continues to rise with players like Square, PayPal, and Fidelity.

Bitcoin or Treasuries or AAA bonds

Furthermore, Bitcoin has no credit risk, as an asset it doesn’t go bust, or get downgraded, like corporations can. So it is better than a AAA bond. What do those yield? Currently 2.33% is the AAA corporate yield. Thirty year Zeros are slightly lower than that, and the Treasury long bond with a coupon is only 1.6%.

Since Bitcoin would have an imputed effective yield (looking at it as a perpetual zero) of around 6.8% down the line, the spread should shrink, Bitcoin’s price should rise even further, by a factor of two or even almost three. That implies a price around $50,000 to $70,000 in a little over 7 years, four or five times the present value and amounts to over 20% per annum compounded.

This is somewhat more aggressive as a projection than the conservative Future Supply Model, which indicates a price around $50,000 being reached in 2030.

Why invest in a corporate at 2.33% or even if interest rates rise, at 3.5%, if you can get a much higher return in a safe asset? There would be an arbitrage opportunity as well of selling the corporates and using that to fund Bitcoin purchases as long as a significant gap remained.

Furthermore, Bitcoin is tax-advantaged, since any gains are capital gains that can also be deferred as desired, rather than dividends that are taxed in the year paid and at a higher rate.

Bitcoin is a highly convex option on a new, emerging financial system. The central banks see it, they are all moving rapidly toward central bank digital currencies. The bankers see it, they are now able to offer custody solutions in the US thanks to a recent OCC ruling.

Long Bitcoin, short bank bonds and collateralized loans?