Which is a Better Digital Asset: Nvidia or Bitcoin?

Exponential Growth vs. Power Law Growth

This is not investment advice. You must evaluate your own risk tolerance and timeframe for any investment.

Nvidia went Exponential ten years ago

Both Nvidia and Bitcoin have suffered corrections in the past week. But both have an incredible track record. Which is the better long-term digital asset and why?

I spent 30 years working in the high performance computing industry, and am a great fan of Nvidia, which is an extremely well run and important company. I have a number of former colleagues in the industry who now work there.

The stock price has been growing at an average rate of 33% (R² of 0.82 for an exponential fit) over the past two decades. But over the past decade it has grown at an astounding average compound rate of 69% (R² of 0.95 for the regression) per annum.

What is the outlook? Well as of today Nvidia’s market cap is $3.1 trillion. They will not be able to grow the stock price at 69% each year on average for the next decade. If they were able to, their market cap would rise to $551 trillion (computation: 1.69¹⁰ x 3.1 T).

This can’t happen, so it won’t happen. All private global wealth is currently about $500 trillion. See https://www.visualcapitalist.com/global-wealth-distribution/ . Global wealth grows about 6.7% per year so a decade from now could be around $1000 trillion. But even with that, Nvidia’s market cap would have to be half of all private global wealth.

Nvidia is an exponential asset, at least for the last decade, as can be seen by looking at the semi-log Chart 1 above. For its first decade after it went public in 1999, the price did not move much, at an average compound annual growth rate (CAGR) of under 5%. But from a decade ago the company really hit its stride and the stock price shot up by the aforementioned 69% average CAGR.

Those of us who lived through the Dotcom bubble and subsequent crash and the Great Financial Crisis know that exponential rises will generally be followed by exponential crashes. And the crash periods are often more accelerated than the rise period.

Kelly analysis of Nvidia and Bitcoin

Imagine you wanted to construct a two asset portfolio holding only Nvidia and Bitcoin, how much of each is optimal? It will depend on the timeframes for rebalancing percentage allocations, but we want to consider the long term, so we look at annual price performance of the two assets.

We start from 2011 when Bitcoin had established price discovery, and look at prices for the two assets as of June 1st of each subsequent year. One sees that Bitcoin outperformed Nvidia in 9 of 13 years. Even starting from 2015 it outperformed in 7 of 10 years.

The Kelly formula looks at the win rate and the relative outperformance in order to determine how much of a portfolio should be put into each asset. One adjusts the allocation as a new data becomes available, using rebalancing at a chosen frequency. This is a high volatility, risky portfolio so one needs to enter into it with eyes open and take a long term perspective, and in this case we consider annual rebalancing.

First we calculate the probability of Bitcoin ‘winning’ vs. Nvidia in a given year, p = 9/13 = 0.692. And q = 1 — p = 0.308 is the loss rate relative to Nvidia. Then we add up all the winning percentages and get a total of 2880% over 9 years, or an average win size w = 320%. For the ‘losses’, the years when Nvidia outperformed, the total was -130% and the average over the four years is l = -32.5%.

Next the Kelly criterion calculates the favorability parameter b = w/(-l) = 9.83; when Bitcoin won, it won big. The optimal Kelly fraction f maximizes an investor’s global wealth over time, and is calculated by:

f = (bp — q)/b = p — q/b = 0.66

In other words the optimal two asset portfolio would be about 2/3 Bitcoin and 1/3 Nvidia. One would not be entirely in Bitcoin because (a) Bitcoin does not outperform in every year, and (b) Bitcoin’s volatility is high (whether in dollar terms or denominated in Nvidia stock) so one wants to be able to put relatively more funds into Bitcoin on pull backs when it falls below the optimal percentage allocation.

By the way, if we restrict to just the last 10 years of returns, we find p = 0.7, b = 2.73, significantly lower for the bparameter, but the optimal f is still 0.59, a 59% allocation to Bitcoin and 41% to Nvidia. (That’s almost a 60/40 ratio, by coincidence.)

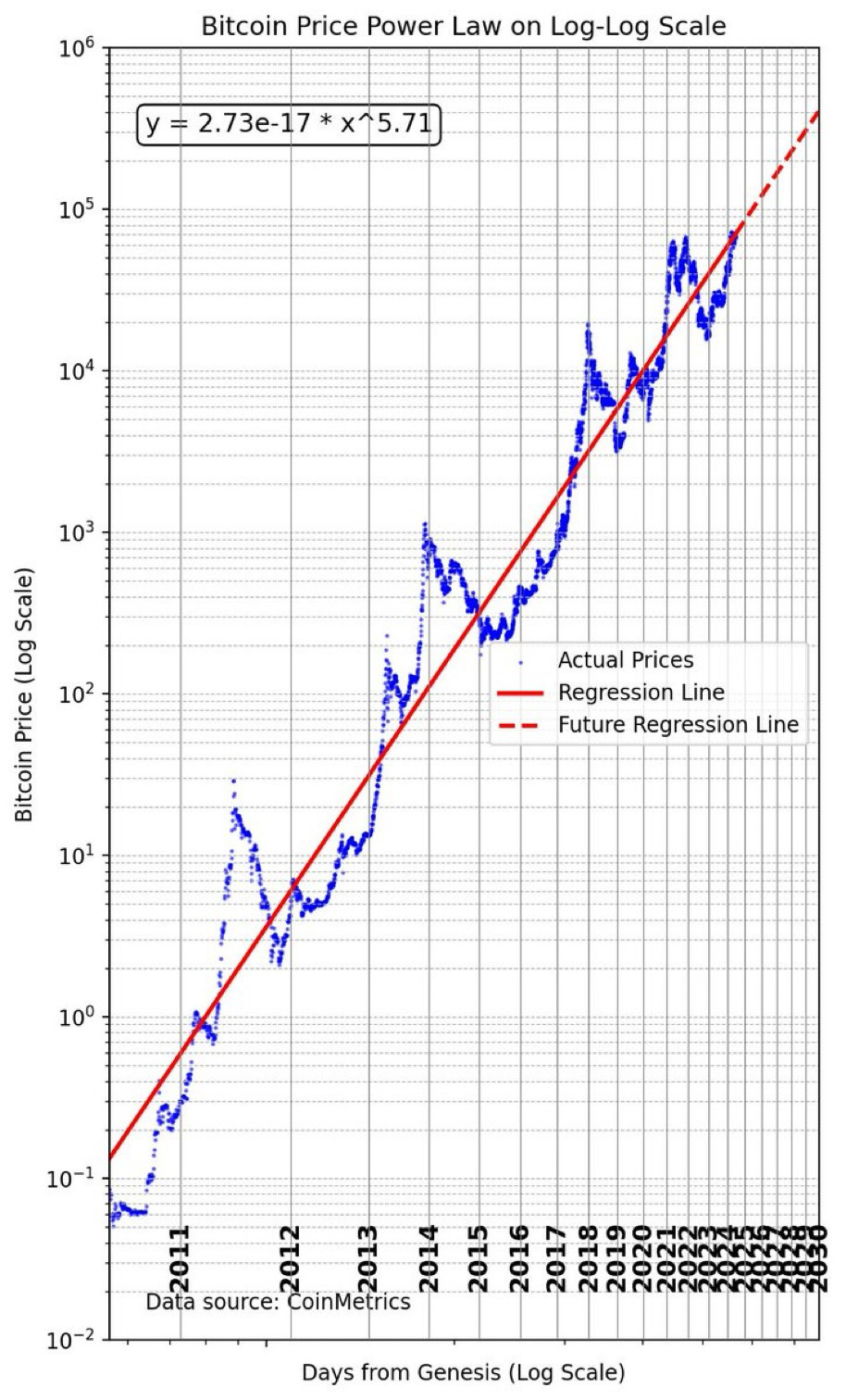

Bitcoin follows a Power Law

When Bitcoin’s price history is plotted on a log-log plot of log price vs. log time, one has a clear straight line; the slope is the power law index of the underlying mathematical relationship. Since as an asset, Bitcoin follows a power law, it intrinsically has more runway than Nvidia.

Power laws appear everywhere in nature, from gravity and electromagnetism to the metabolic rates of animals and the growth of cities. And in particular they apply to networks including social networks; Bitcoin is a monetary network for creating, storing, and exchanging permanent value.

Since it follows a power law, and not an exponential, its returns have been steadily slowing down with time and are expected to continue to do so, while still remaining in the high double digit percentage zone, well above the long-term performance of the S&P or NASDAQ indices. Bitcoin is also becoming more stable as its returns slow. We demonstrate that clearly here: https://stephenperrenod.substack.com/p/bitcoins-growing-stability . The advantage of a long-term power law is that it is less prone to collapse or flattening than an exponential rise.

The Bitcoin power law theory has been developed by PlanG (https://bitposeidon.com) and its power law nature has been separately analyzed and validated by myself and others including @apsk32, @TheRealPlanC, @sina_21st, and @dotkreuger. If we regress Bitcoin in usual Gregorian calendar time, it follows a power law of index 5.7 and if we regress it in Bitcoin blockchain time (52,500 blocks per block year) it follows a 5.4 index power law. Also Bitcoin addresses, wallets of various cutoff sizes, and the mining hashrate all adhere to power laws.

While it is highly volatile, experiencing regular bubble and collapse phases, its volatility is slowing and the underlying power law provides a floor on the downside. Those who haven’t studied it and don’t understand Bitcoin have sometimes said it is like the Dutch Tulip bubble. It has proven them wrong time and time again and now it has reached over $1 trillion in market cap. If it were a tech stock it would be #7 in market cap, just behind Meta (Facebook).

Major institutional money is now being invested into Bitcoin, including several corporate treasuries with allocations in the US and Japan, and 11 ETFs operating in the US since January and several more are active in several international jurisdictions.

Power Laws are different and look different from Exponentials

Exponentials appear as straight lines on semi-log charts, where the y-axis (price) is cast in log terms and the x-axis (time) is cast in linear terms.

Power laws manifest as straight lines on log-log charts using logarithms on both axes, and as curved lines on semi-log charts. For a log-log chart one uses the log of time since an asset began trading. A relationship that goes as the square or the cube, or even a steeper fifth or sixth power will yield a straight line behavior on a log-log chart and the higher the power, the steeper the slope of the best fit regression line.

Above is a log-log chart of Bitcoin based on data from CoinMetrics. The time axis uses a log scale as does the price axis, with time measured from the Bitcoin Genesis block in January of 2009. Thus the labelled calendar years look more scrunched up along the x-axis as one looks to the right.

Power laws are “scale invariant” so when the amount of elapsed time since Bitcoin’s origin doubles then in accordance with the power law, price would go up by a factor of two raised to the power law index, in this case the index is 5.7. A doubling in time projects to an increase in price of a factor of 52. Bitcoin is now almost 15.5 years of age, so one has to wait until around the beginning of 2040 for that amount of price growth, according to the power law projection. That corresponds to a price for Bitcoin of over $3 million; it’s worth the wait.

This is still less of an issue for high valuation than would be another decade of Nvidia’s current exponential growth rate. The market cap of Bitcoin is now $1.2 trillion and it could thus rise to about $60 trillion by 2040. That is just a few percent of future projected total global wealth.

Bitcoin is monetary technology, an alternative to gold, currently $15 trillion market cap, and all national and supranational currencies, whose M2 supply is around $100 trillion. With the historical growth rate of fiat currencies, the global M2 supply could be close to $300 trillion by that time.

Bitcoin is already being used as a reserve asset by some companies, including Microstrategy and several others. Microstrategy’s chairman Michael Saylor sees Bitcoin as digital property and as a major alternative to real estate, stocks, and bonds for investment. It has the potential to be a reserve asset alternative for pension funds (the state of Wisconsin has added Bitcoin already for one fund) and sovereign wealth funds, as well as national treasuries. In such a role, as a sort of “digital gold” one would expect its market cap to be into the tens of trillions of dollars, sufficient to have an impact on a global basis.

The next chart is a semilog chart of Amazon. Here we see exponential boom and bust behavior around the year 2000 as it grew by a factor of 50 in price in a couple of years, and then crashed back by over a factor of 10, losing 90% plus of its value. And this is one of the very best survivors. There were many Dotcom companies that went completely best.

After it recovered Amazon went on to new highs and for over 20 years has had more moderate exponential growth, growing from $0.30 to $186 in the past 22 or 23 years, some 34% as an average compound annual growth rate reaching almost $2 trillion market cap today. Another 20 years of that would put it at well over $600 trillion market cap, again more than all private wealth today. That too is not going to happen for Amazon without significant pullbacks or flattening of the curve.

This is not to say we are in a Dotcom situation for Nvidia. It has a strong leadership position in graphics, HPC, and AI computing and is highly profitable. But it does have some major competition from Intel, AMD, Samsung, Google, and others. Its moats are deep, and it is the clear leader in AI infrastructure for now, but it is not as unique in its own domain as Bitcoin is for cryptocurrency. Bitcoin has no real competition as a proof-of-work digital store of value.

Bitcoin is a better choice

Bitcoin stands alone among proof-of-work digital assets. The #2 proof-of-work coin is Dogecoin and it is responsible for less than 1/10 of Bitcoin’s annually created economic value. Ethereum and other altcoins are not relevant because they do not use proof-of-work, they are more like decentralized companies issuing shares, with a strong preference for insiders, since they use proof-of-stake consensus or something similar with very limited compute power employed.

The proof-of-work consensus required to create Bitcoin and place new transactions in the time chain (blockchain) grounds Bitcoin to real world energy and cryptography, to the tune of over ten GigaWatts of electrical power and 600 Exahash calculations per second. It is this real world coupling, modulated by the difficulty adjustments and halvings of block rewards each four years, that provides a power law support to the network value. So while bubbles develop regularly, typically four years apart for the largest ones, when they deflate they fall back to power law support. Bitcoin’s absolutely fixed supply due to the halvings and its strong foundation that rests on millions of high-performance computing nodes, result in a different form of long-term growth than we typically see with tech stocks.

We believe Bitcoin is a better long-term choice for a “digital asset” investment, and the two-asset Kelly analysis above supports that. Despite the slowing of the power law expectation of annual return, it should remain above 20% per annum trend line growth for another 15 years, through this decade and the next.

Based on Bitcoin’s power law persistence and the likelihood of Nvidia falling away from its 69% compounded exponential rise to more modest growth, I would expect that Bitcoin’s market cap will be higher than Nvidia’s by the end of the decade, and perhaps in the neighborhood of $5 trillion. That may even happen during this halving cycle that lasts four years and began this April.