This is not investment advice. Bitcoin is highly volatile. Past performance of back-tested models is no assurance of future performance. Only invest what you can afford to lose. You must decide how much of your investment capital you are willing to risk with Bitcoin. No warranties are expressed or implied.

Bitcoin as Digital Gold

Bitcoin is often referred to as a sort of digital gold. It is a monetary asset, but unlike gold, it is not mined and minted into physical coins or bars. Instead, it is mined by supercomputing farms of specialized cryptographic solver rigs, and imprinted onto a permanent ledger, the time chain (or blockchain). The winning rig for a particular block receives a block reward composed of a subsidy and transaction fees. For Bitcoin, the subsidy is cut in half each four Block years of 52,500 blocks’ duration, each slightly shorter than a calendar year.

Figure 1. Monthly data for BTC price in ounces of gold over seven plus years and best fits for an exponential model (green) and a power law model (gray).

Bitcoin’s price has generally been rapidly rising when measured in terms of the gold price as well as fiat currencies.

I have performed a regression on monthly data from April 2013 to September 2020 of the price of Bitcoin denominated in ounces of gold, looking initially at three different model relationships.

I quickly discarded a linear model because it is unphysical, with negative price predictions early on, and a much lower correlation coefficient than two more reasonable models.

Exponential and Power law models

These are simply two parameter models; each has a slope and intercept parameter. The first one is an exponential model with the log of price increasing linearly in time. The time is measured in years elapsed since the beginning of January 2009, when the first Bitcoin block was mined.

The second model is a power law of log of price vs. log of time elapsed. We use log10 in the following, rather than natural log, for ease of mental arithmetic in the conversion to linear price.

The time interval runs for almost seven and a half years, from y = 4.25 to 11.67 years, where y = time elapsed since 2009 January 1st, in years. There are 90 sets of data points. The best fit curves for both models are plotted in Figure 1 against the monthly Bitcoin/gold price ratio.

The models exhibit squared correlations of R² = 0.81 (0.80) for the exponential (power law) model, respectively, and the F-values are 375 (345). The respective Akaike information criterion values are -219 (-213). Based on these statistical measures, one can not favor one model over the other at this point.

The exponential model is log10 (P) = 0.27*y-2.11; thus the value of Bitcoin in gold terms increases by a factor of 10 roughly each 4 years with this model. The current model fair value is 10.5 ounces versus an observed value on the 1st of September 2020 of 6.04 ounces of gold value per Bitcoin.

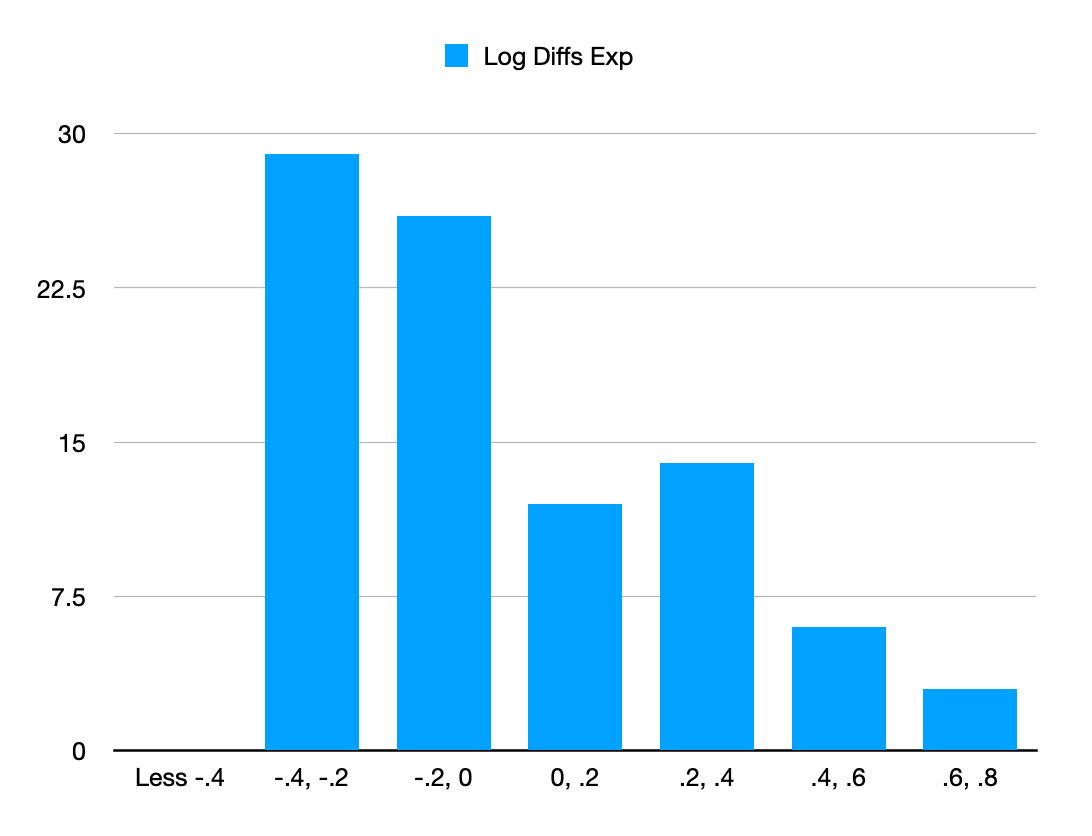

Figure 2. Distribution of the differentials of log10 price for the exponential model best fit (negative when price is below the model). The distribution is highly skewed with 61% of the data points negative and a long right tail.

The power law model is log10 (P) = 4.61 log10 (y)-4.05 (or P = y^(4.61)/11220 in ounces of gold; value relative to gold increases more than the fourth power of time since 2009). The power law's current fair value is 7.44 ounces of gold.

Figure 2 shows the binned differentials for log10 of price — model forecast for the exponential model. One sees that the differentials are quite positively skewed. The largest value is about twice the absolute magnitude of the minimum value. The Pearson skew estimate is 1.02 and the skewness is 0.80. The standard deviation in log price is large at 0.283 in the log or a factor of 1.92.

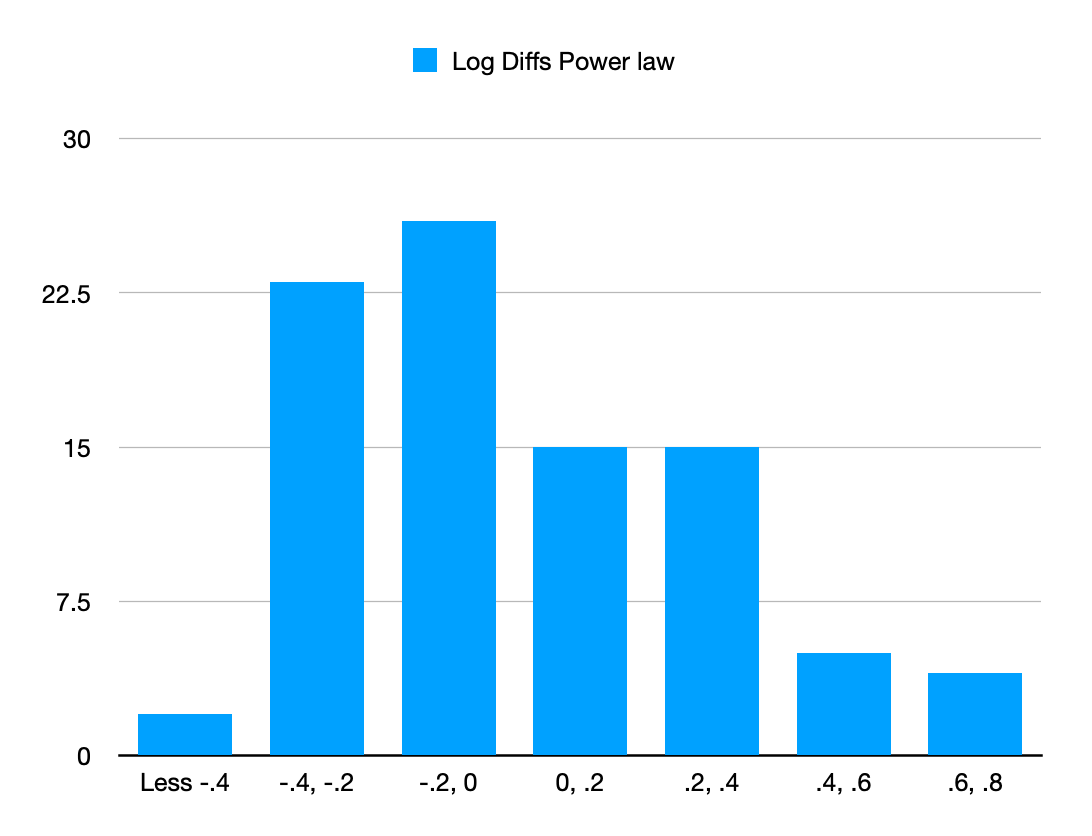

Figure 3 shows the differentials of price-model forecast for the power law model. The Pearson skew estimate is 0.44 and the skewness is 0.52, the standard deviation is 0.293 in the log or a factor of 1.96.

So volatility is high as is obvious from visual inspection and around a factor of 2 from the fair value projections.

As a general rule, one could favor Bitcoin purchases over gold when it is below the fair value price and benefit from the positive convexity as displayed by the skew of the residuals.

Figure 3. Distribution of the differentials of log10 price for the power law model. The distribution is highly skewed with 57% of the data points negative and a long right tail reflecting the two strong price spikes at y = 5 and y = 9, following the first and second Halvings.

Forecasts for 3, 6, 12 Months

Table 1 below shows the twelve-month forecast for the two models, as well as the three and six-month projections for fair value. We should have a pretty good sense if one of these models is performing better than the other within one year, since the exponential model predicts almost 20 ounces for the Bitcoin price a year from now, as opposed to 11 ounces for the power law model. The exponential model has the price in gold terms rising much more rapidly, at around 0.75 ounces per month over the next year, while the power law model rise is significantly lower, around 0.29 ounces per month. I also show the more speculative projections out to 2030.

The more conservative power law model indicates a value of more than 100 ounces and about $220,000 worth at the present gold price. The exponential model goes a bit wild, at over 3000 ounces, and over 100 kilos of gold per Bitcoin. It implies a market cap for Bitcoin that would exceed $100 trillion, over ten times the value of all gold, and above today’s global money supply.

So overall, I favor the power law model. Of course, the parameters for the models will evolve with time.

Bitcoin now has a stock-to-flow parameter of 56, essentially equal to that of gold. However, unlike gold, its new forward supply relative production is more limited, due to upcoming Halvings in 2024 and 2028 that will push the stock-to-flow to 120 then to 248 and then “to infinity and beyond.” The remaining Bitcoin will be released at an ever slower rate over the next 12 decades.

Gold is rare because it can only be made in supernovae and must be recycled through the interstellar medium; Bitcoin is rare because its monetary policy is the hardest ever, with 18.5 million (88%) already produced out of a maximum 21 million. With 151 Exahash/s of mining power, it’s a game for supercomputers.

Gold adoption is mature, with thousands of years of cultural history. Some 12% of Americans own gold for investment purposes, but just 5% are estimated to own Bitcoin. Bitcoin’s convenience and adoption keep rising. Relative to gold it is more transportable, more divisible, easier to audit and assay, and less expensive to store. It can be sent across the globe in less than an hour.

The value of all gold is around $10 trillion, the value of Bitcoin only $0.2 trillion, so there is easily a factor of 10 or even a factor of 50 of potential upside. A factor of 10 would place it at 20% of gold’s market cap even if gold does not rise in value further. A single Bitcoin might reach the equivalent of two or three kilograms of gold if the rise continues for another multiplicative factor of 10 or 15. The power law model shows this could occur before the decade of the 2020s is over.