I have analyzed 14.3 block years’ worth of residuals (differentials) between the best fit power law and observed monthly price action.

The differentials are in log10 of price since Bitcoin’s volatility is so high. The minimum value is -0.49 and the maximum 0.84 in the logarithm (corresponding to a factor of 3.1 on the downside and a factor of 6.9 on the upside as departures from the power law trend).

Figure 1. A histogram of Bitcoin’s block monthly price vs. power law fit residuals in log10 terms. Note the sharp cutoff in the left tail around -0.4 and the smooth right-tail skew to higher absolute values than the left tail.

But residuals are coming down with time. The standard deviation for the full data set is 0.31 and for the most recent four years (48 block months) it is 0.24.

These values correspond to multiplicative ratios of 2.05 and 1.74 respectively. That is, suppose fair value on the power law trend is $60,000, then one sigma below is about $30K and one sigma above would be about $120K. If one uses the smaller value from only the most recent four years, the one sigma range is about $34K to $104K.

Actually the residuals are skewed to the right (positive) tail and it is unusual to see prices less than one sigma below trend.

The power law best fit in block years is currently $54,800 (B/16)^5.4 and we are now at B = 16.38 block years, so the trend fair value is $62K. It would be surprising if Bitcoin fell below $62K/1.74 = $36K from here, even ignoring that we are in the favorable part of the approximately four-year cycle.

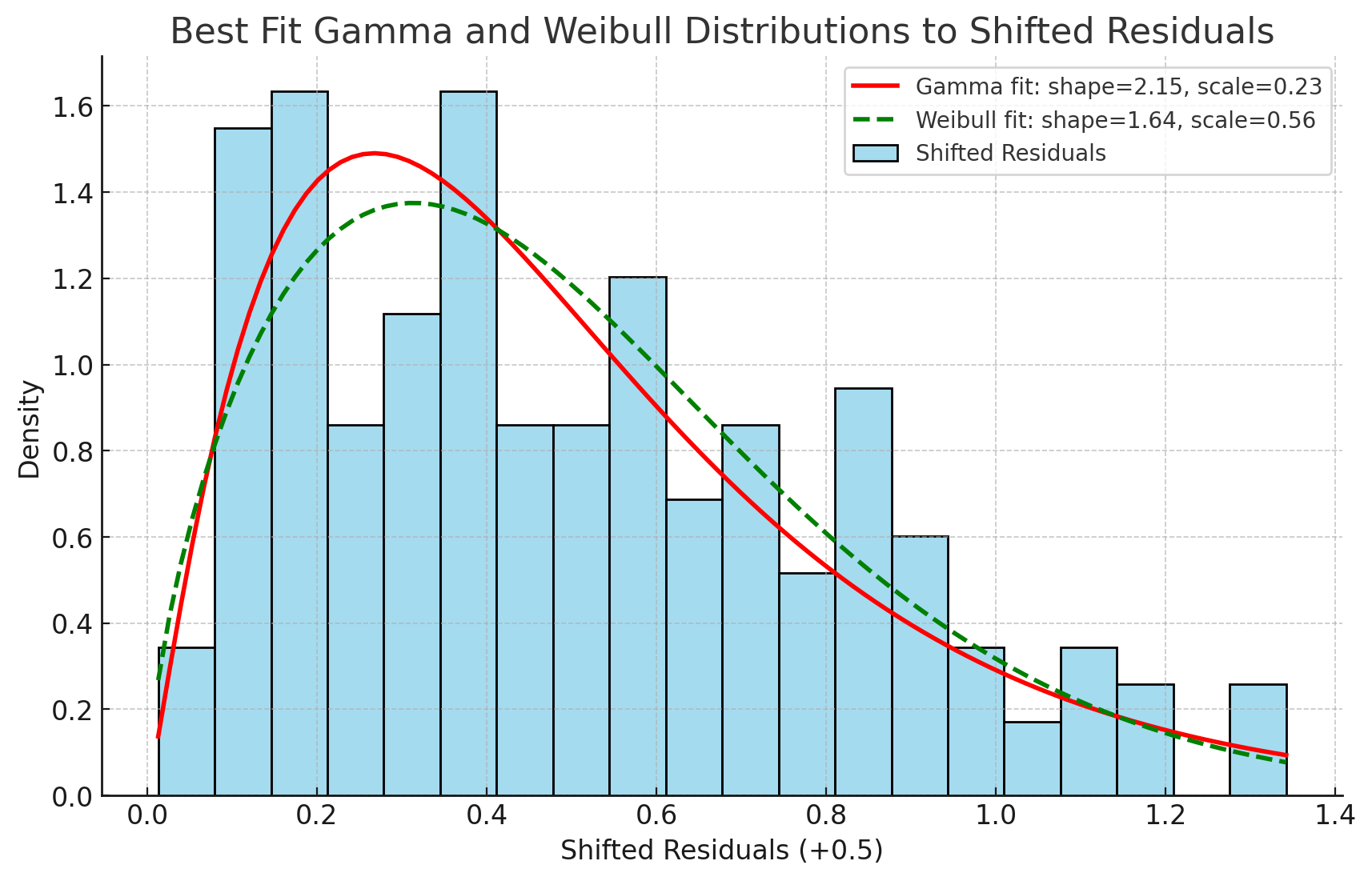

We looked at 6 possible analytical model fits to the histogram. In order to make all of these various forms addressable, the data has all been shifted by +0.5 in the logarithm base 10 for analysis.

We looked at Gaussian, skew-normal, log-normal (of log data!) and Laplacian distributions, none of which were good fits, and then our two winners, the Gamma distribution of the Weibull distribution.

While both are acceptable, Weibull gives a somewhat better fit after evaluating the Chi-square and Kolmogrov-Smirnov tests and the Akaike Information Criteria for both. For the Weibull the chi-square is 24.9 with 173 degrees of freedom, the K-S p-value is 0.75 (a very good fit), and the AIC at 58 is somewhat lower than for the Gamma distribution.

According to ChatGPT “Both distributions show reasonable fits, with the Weibull having a slight better overall fit”.

Figure 2. Weibull and Gamma best fit distributions. The residuals have been shifted by +0.5 to assist the analysis. Both are good fits; the Weibull is somewhat better.

The Weibull distribution has a shape parameter of 1.64 and a scale parameter of 0.56. Just 7.5% of the area under the Weibull curve is contained in the region above 1.0 for the shifted residuals, or above 0.5 for the unshifted.

This is different from the Weibull CDF that can be used for S-curve tests against Bitcoin price that I have written about previously and that start out as a power law and that also indicate that a power law is sufficient for now to describe Bitcoin’s price development.

The chart above shows the Gamma and Weibull distribution best fits to the shifted data. Both capture the sharp cutoff on the left and long right tail of the actual distribution.

The value of the last residual in the data set is -0.015 and is at the 54th percentile, near the median. There is lots of upside remaining, to about 0.6 in the first histogram or 1.1 with the shifted data, at the 95th percentile. That is a factor of 4 above trend.

Given that volatility is dropping with time one might not want to press one’s luck beyond about 0.5 or a factor of 3. The recent four years’ standard deviation being 1.74 as the multiplicative factor corresponds to a factor of 3.03 (1.74 squared) price above power law trend at the two sigma level. The 10%, 20%, 50%, 80%, 90% levels are at -0.38, -0.30, -0.04, 0.29 and 0.41 on the first histogram. Caution would say do not expect much excursion beyond the 80% level given that long-term volatility is decreasing.

What does a Weibull distribution for residuals mean in the context of a power law? The long right tail is a consequence of the exponential bubbles and crashes that occur on a roughly four-year long cycle. Whether these are due to the Halving cycle or global macro liquidity cycles is an unresolved issue.

Residuals following a Weibull distribution suggests that there are multiple phases or regimes and/or threshold effects at play. We know that Bitcoin, in addition to exponential bubbles, has a threshold effect or price floor-like behavior which could be due in part to miner capitulation at low prices, as well as elimination of speculative trader balances. Usually hashrate follows price, but in Bitcoin winter this causality can reverse.

The Weibull shape parameter is k = 1.64 and ChatGPT 4o says this suggests residuals can grow larger over time, bubbles can become more extreme or frequent. The bubble deviations may be linked to cycles in market behavior. The Weibull is consistent with rapid bubble growth and sudden corrections. ChatGPT says: “The power law model is generally effective during normal growth phases but breaks down during bubble formation and bursting.”