Bitcoin and Shrinking Populations

Decreasing Population is Baked in — Bitcoin Economics are more Suitable

For the first time in human history, global population growth is ending. Fiat monetary systems were designed for continual demographic expansion, but will struggle in a world defined by aging slower growth, and capital abundance.

This trajectory is now reversing. The population of the Earth is three times larger than when I was born, but it will peak in the second half of this century and then enter prolonged decline. an Estimates from the United Nations and other forecasters typically place the peak in the 2070s or 2080s. The wild card is the degree of life extension achievable in the next few decades, but the benefits will not come all at once, will aggravate the increasing tilt toward older demographics.

The primary drivers of decreasing fertility outcomes are well understood: (1) urbanization, (2) women attaining higher levels of education and employment participation, leading to (3) delayed marriage and later childbirth.

A number of mid-sized and larger countries already have shrinking populations:

China — 1.4 billion

Russia — 146 million

Japan — 120 million

Thailand — 71 million

Italy — 59 million

South Korea — 51 million (has world’s lowest fertility rate)

Ukraine — 38 million

Poland — 38 million

Taiwan — 23 million

Romania — 19 million

Greece — 11 million

Portugal — 10 million

Many more nations will join the list in the next few decades. East Asia and Southern Europe are in demographic decline at present, and most of the world sits below the replacement fertility rate of 2.1 children. Few countries are above replacement rate outside of those in Africa and South Asia.

Fiat systems depend on growth, with more demand and more borrowing. And with excessive money creation by governments in an attempt to service their own debt while also providing sufficient liquidity to their economies, capital misallocation by the private and public sectors increases. The number of zombie companies tends to grow, productivity suffers, and financial crises become more frequent and more severe.

Aggravating this problem, the global working population will peak much sooner, perhaps within the next 20 years, and it has already peaked in high income economies. Heavier debt burdens, rising retirement dependency ratios (retirees to workers), along with slower overall growth have been continuing challenges across the developed world since early in this century.

Bitcoin is Better

Bitcoin has arrived at a propitious time with regard to the demographic collapse. It is superior monetary technology, that conquers both space and time. It can move around the globe unfettered within an hour and is designed to preserve and increase value over time. It is the first monetary technology with an absolutely fixed supply and easy open-source audibility, making it the first scientifically precise standard for money in history, with 15 digits of divisibility.

One objection to Bitcoin is that the supply is not elastic, implying real economic growth would have to be accommodated by falling prices. But we are already very familiar with that in many domains, notably technology where Moore’s Law has provided around twice as much for the buck every couple of years.

If the population itself is shrinking, why should the number of monetary units expand? The global M2 money supply grows at around 7% a year, doubling each decade. With Bitcoin and a shrinking population the money supply per capita would increase at the same rate as population decline (reversing the sign).

Bitcoin scales with capital and is well designed for nations with aging societies and excess savings relative to those nations with younger populations and thus high consumption due to growing families.

After the population peak, growth will need to increasingly come from capital reallocation and productivity gains, especially from AI and other automation advances. There will be persistent pressure on energy, land, materials but growing abundance in software and services.

It appears that AI could concentrate wealth toward capital owners, data center providers, and energy suppliers. But Bitcoin, including with support from AI, can disintermediate much of the rent-seeking seen today in the FIRE industries (finance, insurance, real estate). AI could boost growth rates, but has to work against the drag of an older population that will need more and more health care due to the very breakthroughs that AI will facilitate in the medical field.

Bitcoin is about capital preservation and honest exchanges, with value preserved across time. Productivity gains relative to the hurdle rate of Bitcoin are expressed in lower real prices, rather than asset inflation.

Power Law

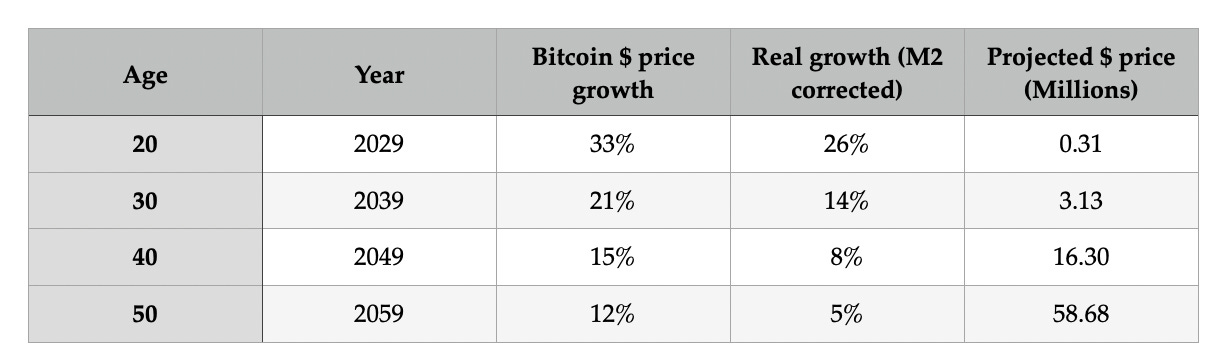

Right now the Bitcoin hurdle rate is very challenging but it should come down steadily with time given the persistence of power law behavior of Bitcoin’s price. To first order annual growth can be computed as k/T where T is the Bitcoin blockchain’s age and k is the power law slope. Using k = 5.74 as indicated by a t-location-scale analysis of over 360,000 data pairs, drawn from the full price history, one can then compute the growth rates and prices in Table 1.

Projects with real returns in single digits become feasible with the more reasonable hurdle rates after 2045. As we approach mid-century, the required real return from Bitcoin’s growth trajectory is more compatible with long-duration energy and infrastructure investments.

On this trajectory Bitcoin’s market cap could be of order $1 quadrillion in a world with nominal wealth of perhaps as much as $10 quadrillion. Bitcoin could then function as a dominant capital denominator, although to what extent currencies would be tied directly to Bitcoin is an open question.

A Bitcoin-anchored system implies capital can become relatively more abundant but projects will need to surpass real hurdle rates. There should be less leverage, less speculation, and less malinvestment in a Bitcoin-centric capital system. Real interest rates could be lower and more stable, with capital investment grounded to real productivity growth rather than artificial credit expansion.

“In a world where global population peaks and then shrinks after ~2075, a Bitcoin-anchored system is more sensible than fiat because it supports savings-backed credit, stable real rates, and capital preservation without requiring perpetual demographic or debt expansion.” - ChatGPT 5.2

Which Nations First

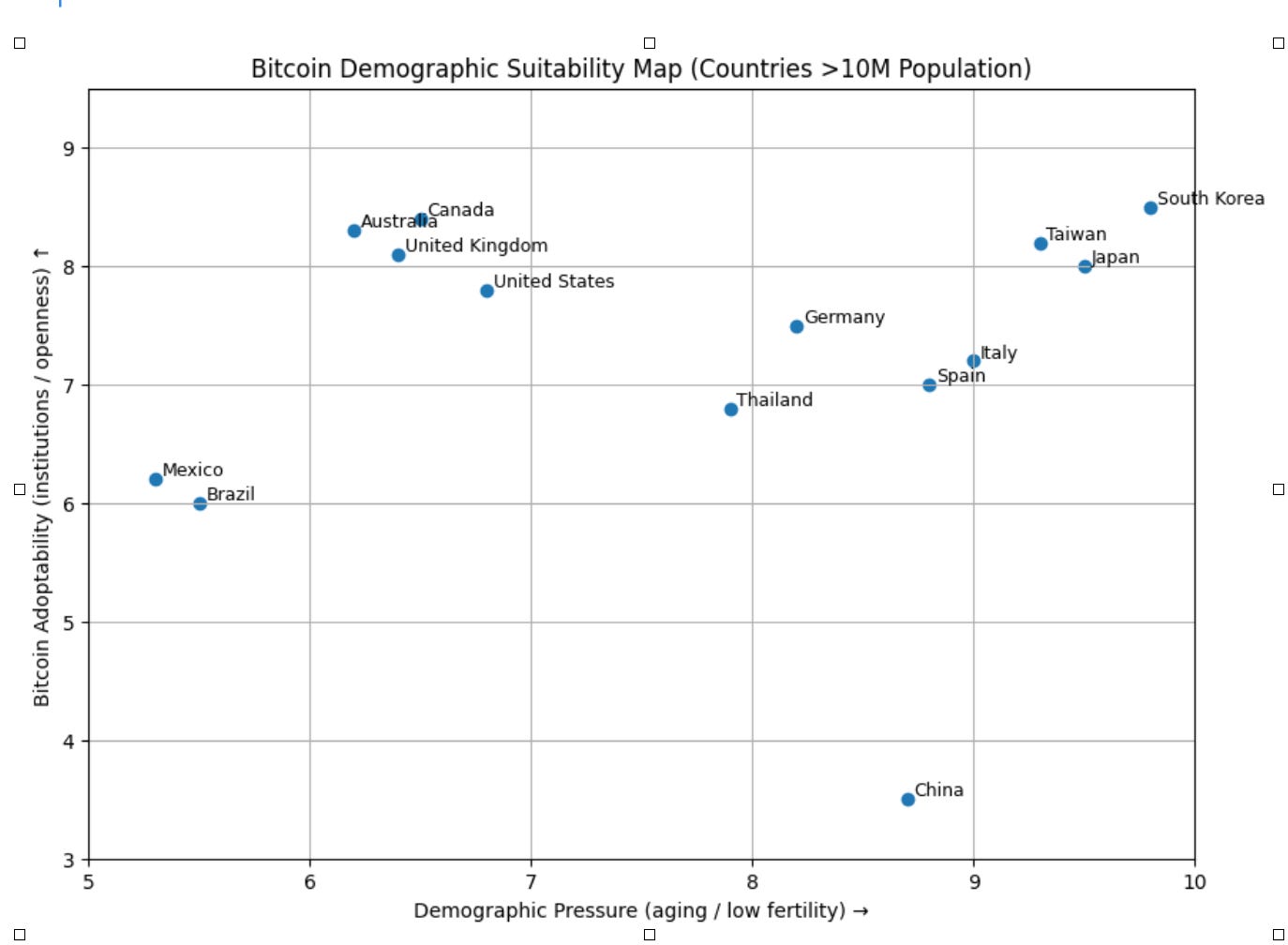

If we believe that Bitcoin is especially well suited to low-growth environments with aging and then falling populations, the natural question is to which nations will that first apply? In addition to the demographic criteria, it is also necessary to consider which political and economic systems are open to the prospect of greater Bitcoin adoption.

The aging, capital rich, and low-growth societies such as those in East Asia are clear candidates for early adoption. These economies are known for their high savings rates and capital formation. The next obvious group of candidates are found among the nations of Southern Europe: Portugal, Italy, Greece, and Spain.

Most of these economies have open capitalist or mixed economies. The notable exception is China. China is ranked low on openness; they have strong capital controls, a restrictive financial regime, and are promoting the Yuan including in its CBDC form for their Belt and Road, thus widespread adoption to Bitcoin by the sovereign or large Chinese corporations is quite unlikely without major reforms.

The figure below is a categorization of a number of countries on the two axes of openness to Bitcoin (y-axis) and demographic favorability (i.e. ‘poor’ demographics, x-axis). On sees that East Asian and Southern European nations have the most favorable environments (upper right corner). The Anglophone countries cluster high on openness but also have less challenging demographics than East Asia and Europe.

In a nutshell, younger economies like India, Indonesia, and Nigeria are adopting Bitcoin primarily for payments. Aging, capital-rich societies are likely to adopt it as a monetary foundation, the ultimate asset for preserving capital in personal savings, in company treasuries, and by pension funds and for deploying as long-term stable investment capital.

A Bitcoin economy does not depend on population growth, continually rising debt, or perpetual inflation. It is the antidote to these dependencies.

Bitcoin stabilizes capital in a world where demographics no longer do. - ChatGPT 5.2

"Bitcoin stabilizes capital" — quoting ChatGPT. Meanwhile in reality, Bitcoin ETF investors are underwater, mining costs exceed the price, and corporate treasuries are sitting on billions in unrealized losses. The theoretical elegance of fixed supply meets the practical reality: who's making money here? The people selling the thesis, not the people buying the coin. Where are the customers' yachts? https://www.mecrankyoldguy.com/p/bitcoin-in-your-401k-where-are-the

Interesting article.

https://jinlow.substack.com/p/bitcoin-price-analysis-2026-the-geopolitical